Do you need a fiscal representative in Portugal?

The landscape of fiscal representation in Portugal underwent a significant transformation in 2022, providing a substantial relief to non-residents, particularly those from outside the EU/EEA.

As per the updated Portuguese law, individuals residing in third countries can forego the obligation to appoint a tax representative. This exemption applies if they subscribe to any of the dematerialized notification channels. These channels include the system of electronic notifications and quotations available on the Finance Portal, or the electronic mailbox.

Simply put, as a resident outside the EU/EEA, you can now own a property or a car in Portugal without the necessity of a fiscal representative, provided you’re subscribed to these digital notification channels.

This is a substantial shift from the past when fiscal representation was mandatory for such transactions.

Worth Noting: The appointment of a tax representative for residents of the European Union or the European Economic Area (Norway, Iceland and

Liechtenstein) has been optional, even preceding this tax change.

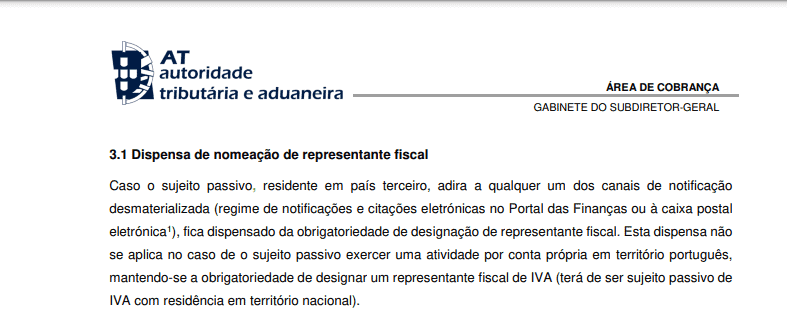

According to the Circular Letter no. 90057 of 20 July 2022, an exemption has been outlined for non-residents subscribing to any dematerialized notification channels.

Here is the relevant extract in full:

“3.1 Exemption from appointing a tax representative: If the taxable person, residing in a third country, subscribes to any of the dematerialized notification channels (system of electronic notifications and quotations on the Finance Portal or the electronic mailbox), he/she is exempted from the obligation to designate a fiscal representative. This waiver does not apply if the taxable person carries out a self-employed activity in Portuguese territory, maintaining the obligation to appoint a VAT tax representative (must be a VAT taxable person residing in national territory).”

Here’s the tutorial on activating dematerialized notification channels from official Autoridade Tributária e Aduaneira Youtube channel:

So, in simpler terms, this means that any non-EU/EEA resident can own a property or a car in Portugal without the need for a fiscal representative, as long as they are signed up to these channels.

However, if the individual carries out a self-employed activity on Portuguese soil, they are still required to appoint a VAT tax representative residing in Portugal.

It’s crucial to note that not all companies are up-to-date with these changes. Some are still operating under the old rules, charging clients for fiscal representation.

Here at Novomove, we’ve tailored our NIF service to align with this new law, removing the need for a fiscal representative and its accompanying costs. This streamlined approach offers an attractive option for those wishing to simplify their procedures and avoid needless expenses.

For a more in-depth understanding of these changes in the tax law, you can refer to these official documents: